06 Apr How to Prepare for a Recession in 2026

A couple years ago, the warning signs of a recession were mostly talk. But in 2026, this concern is much higher and if you aren’t preparing for it now, you will not be ready.

With the Iran war, tariffs, and general economic uncertainty, the likelihood of a recession in the United States is much higher now.

Consumer confidence in the future is lower, the impact of rising fuel prices will slowly permeate the economy, and immigration policy continues to have far reaching effects. Moody’s AI recession model is at 49%. It’s trained on 80 years of data and when the model hits 50%, there’s been a recession within 12 months.

If you are concerned about a recession, here is what you need to do.

Table of Contents

💡 The principle behind each of these is simple – the biggest worry in a recession is that you lose your job and are unemployed for a long time. To hedge against this, you have to increase your savings and have a cash cushion to weather that storm. The longer the better. When the situation changes and your worry subsides, you can invest the extra savings or use it to pay down debt.

Increase Your Emergency Fund

Your emergency fund is your first line of defense against any financial problem – and one of the biggest financial problems is losing your job.

During a recession, the probability of that goes up. And the time it takes to find a new job goes up too. The Bureau of Labor Statistics keep track of this and this charge showed what happened after the Great Recession in 2007-2009. 20-22 weeks is a long time.

This is why the number one suggestion is to increase your emergency fund.

- 🌞 Standard advice: 3-6 months of expenses

- ☔ Recession advice: Aim for twelve months – you don’t know how long the job search will take.

Then, put that cash in a high yield savings account so you’re maximizing the interest you’re earning while it waits (hopefully never to be used). If you want slightly higher yield, you can also look at CDs (we like CD Valet because they list 30,000+ rates)

📩 Want a free email mini-course that walks you through how to build your emergency fund?

Avoid Big Purchases

Big purchases will either saddle you with debt or take a bunch chunk out of your cash savings – both of which are bad at a time when you think the economy may be shrinking.

If you must make a big purchase, downsize it.

- Need a car? Consider a used one.

- Thinking about buying a house? Maybe rent a bit longer for flexibility.

If there is a recession, chances are you will be able to find yourself a good deal. Interest rates will come down, making mortgages more affordable, and your stockpile of dollars will be an asset.

💡 As a corollary, you can reduce the amount you’re paying to your debts as long as you’re banking the savings and those debts are relatively low interest. If you’re aggressively paying down high interest credit card debt, it’s safe to keep doing that because your worst case scenario is that you’d be charging more to your cards. If you have lower interest student or mortgage debt, it may make sense to save the difference for now in case you need it.

Renegotiate Your Debt

If you have any debt, especially high interest debt like credit card debt, try to renegotiate it. The best example is high interest credit card debt, call them to find out if you can get better terms such as a lower interest rate. If you can lower your rate, that will lower how much you pay each month and give you more breathing room.

If a recession does occur, use it as an opportunity to refinance because rates tend to fall during a recession. Refinancing, such as a mortgage, typically comes with a cost so you will want to do the math and ensure you come out ahead.

While you’re at it, see if you can increase your credit limit as this can help your credit.

Add Income Diversification

Think of a side hustle as income insurance. It gives you extra cash to bolster your emergency fund, pay down debt, or just give you piece of mind that if you lose your job, you’re not going to zero.

There are many side hustles you can pursue (here’s a list of online jobs to consider) and they don’t require you to drive for Uber/Lyft or deliver food for Doordash/Instacart (those those are great side hustles).

You don’t have to make a ton of money to make a difference in your financial situation.

Keep Saving for Retirement

You may be tempted to reduce your retirement contributions. Resist the urge.

At a minimum, contribute enough so you get any company matches so you aren’t leaving any money on the table.

You want to continue saving for retirement because a recession may never come, or you may not be affected by it, and you want to ensure your goals in the future are still being pursued. Don’t sacrifice your future for something that might not happen.

Be Realistic About Your Risk Tolerance

If there is a recession, the stock market will fall. The Great Recession is an extreme example but if you look at the list of stock market crashes and bear markets, it’s pretty gnarly (and there were a lot of “crashes” in the last few years that didn’t ring alarm bells here).

Ask yourself honestly:

- What if my portfolio dropped 10%, would I be ok?

- What about 20%?

- Or more?

You may want to change your asset allocation if it will keep you up at night. Again, I don’t recommend making decisions based out of fear but only you know what you’ll be comfortable with.

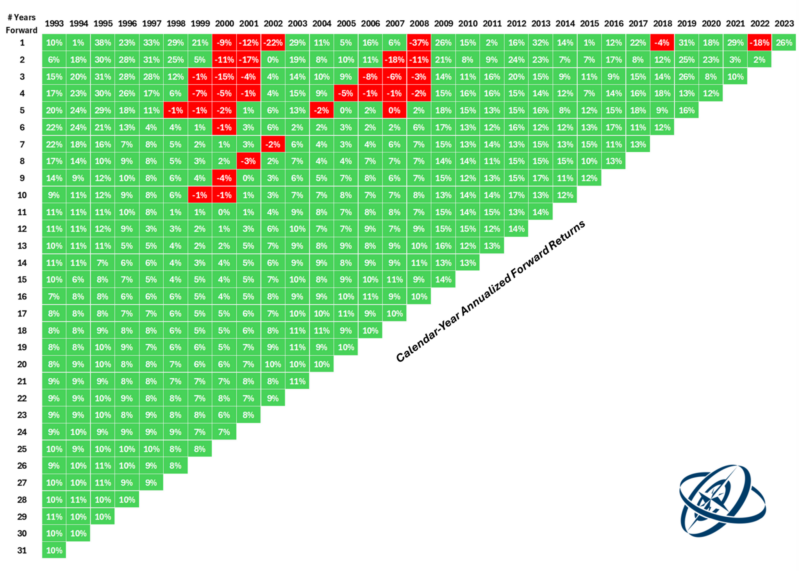

If you want to feel better about it and can financially navigate the market falling, look at this chart from A Wealth of Common Sense. It shows the annualized return of the S&P 500 looking forward.

So if you look at the 2000 column, it returned (on an annual basis) -9% after one year. -11% after two years. But by year 7, it had recovered enough that you had a 1% annualized return for each of the prior 7 years (so it more than recovered).

The point of this chart is how little red there is and how quickly things recover. Use it to calm yourself, it’s what I do. 😁

Start or Update Your Budget

If you don’t budget at all, a free budgeting tool can make this really easy.

When times are good, not knowing where every last dollar goes isn’t as critical. When times get tougher, you want to batten down the hatches and make sure your budget is tight. No wasted dollars that could be put into your emergency fund.

Also, if you lose your job, you will know where to cut expenses ahead of time.

Review Your Emergency Plan

We know about emergency funds but have you create an emergency plan? It’s a fire drill for potential emergencies, like losing your job, which are easier to make when your house isn’t on fire yet.

Work through these questions now:

- What will you do if you lose your job?

- Where do you go to file for unemployment?

- Where will you submit your resume? Have you updated it?

Is there anything you can do right now that may help your prospects in the future? Does that mean attending networking events or learning how to find a job today?

What if you’re out of a job for longer than the number of weeks your state offers unemployment benefits? Will you do side gigs? Set some of those things up now (and perhaps give them a try to see if you’d even like them, the extra cash can go towards your savings).

Preparation is Power

Preparing for a recession doesn’t change the odds that it’ll happen – but it does put you in a better position to navigate one.

And if it doesn’t, you have extra savings that you can put towards your other goals or invest them in your future.